Let’s cut to the headline takeaways:

- One of the single biggest causes of the current inflation is the pandemic and the breaks in global supply chains that resulted. In a capitalist system, or any “market” system, when supply is restricted and demand remains high, prices rise.

- The second biggest cause is the U.S. “Cold War 2.0”—geopolitical economic policies directed against Russia and China, and any other country unwilling to submit to U.S. domination tactics. Sanctions, tariffs and warfare are especially damaging energy markets, which drive up costs throughout all world economies.

- A third factor greatly aggravating inflation is the domination of many markets by large corporations.

- Uncorrected inflation can cause markets to collapse, and political systems, too. Markets do not self-correct from collapse, except in right-wing dream theories. Major public intervention is required to bring supply and demand back in balance, and avert the enormous human costs of collapse.

- The solutions, in outline are pretty clear:

- Worldwide collaborative efforts to stem the pandemic, which is not over yet.

- Ending Cold Wars. Embrace peaceful coexistence.

- Publicly-directed energy investment, including partial or full public takeover of the too-big-to-fail energy corporations

Those are the headlines. The common thread underlying each of these causes is the dominating position of U.S. monopoly capitalists over the U.S. government, and by extension, the world economy.

It must be ceded in advance that, while most economists are in agreement about the central role of the pandemic in triggering a supply chain breakdown, there is no firm consensus among them regarding what policies should be implemented to address inflation.

Those like Larry Summers serving a GOP big business agenda blame rising wages. Others using a more progressive lens, such as the Economic Policy Institute, Robert Reich, or Joseph Stiglitz, identify monopoly-driven price-hiking as the main source of the problem.

Receiving significantly less attention is the fact that most of the developing world blames U.S.-led Cold War 2.0 policies.

It is difficult to convey the intensity and scale of antagonistic and turbulent economic forces currently in motion. This adds uncertainty to nearly all outcomes.

Given the present balance of forces, the policy changes within reach may not remedy the fundamental causes of the current inflation problem. However, this piece asserts that stopping the Ukraine war sanctions and counter sanctions is a vital remedy in the short term.

Most economists are in agreement about the initial cause of the inflation spike: large supply chain disruptions from the COVID pandemic. A billion workers became ill. Millions died. Family and other impacts of the pandemic made it impossible for many to return to former work.

Labor is the source of commercial value. The loss of those workers raised costs everywhere: materials, services, parts, transport, and labor itself were not (and still are not) sufficient to meet demand. One may ask, why has demand remained so high?

The answers are a) because governments injected a huge amount of cash into the pockets of the public (alongside considerable corruption); and b) the Internet infrastructures enabled an unexpected shift to remote work for many occupations.

About “Externalities”

The pandemic is an example of what bourgeois economists call an “externality”—like bad or good weather, pollution, war, acts of God, etc.

The pandemic is an example of what bourgeois economists call an “externality”—like bad or good weather, pollution, war, acts of God, etc.

For the most part, bourgeois economics disposes of externalities by means of taxes: the public pays the government to resolve contradictions in the system, including problems (like waste or rising CO2 levels) which are frequently created by privately-owned companies.

Meanwhile, U.S. corporations are limited liability firms. That means company owners may not be forced to cover business liabilities from their personal fortunes, though such fortunes are clearly derived from those entities. However, disputes arise almost everywhere regarding who should pay when various social and environmental costs arise.

Marxists would not call most of these “external” to market forces, since many instances of such “externalities” (polluted rivers, for example) are direct consequences of ordinary market forces. They have large costs that must be consumed by the public—i.e., the state—in one form or another. Otherwise, the liabilities would wreck markets with either extreme inflation, deflation, or collapse (where no trading is taking place).

However, the policy changes at hand may not remedy all the fundamental causes, but only provide the “less worse” option. This can muddy the political consequences.

In addition, the Ukraine War and the resulting sanctions regimes killed all prospects of recovering from COVID-related energy shocks. From Mike Roberts on the left, and the Fed itself on the Center-Right, there is wide agreement on that, although not much mention of it through all the purple imperial haze.

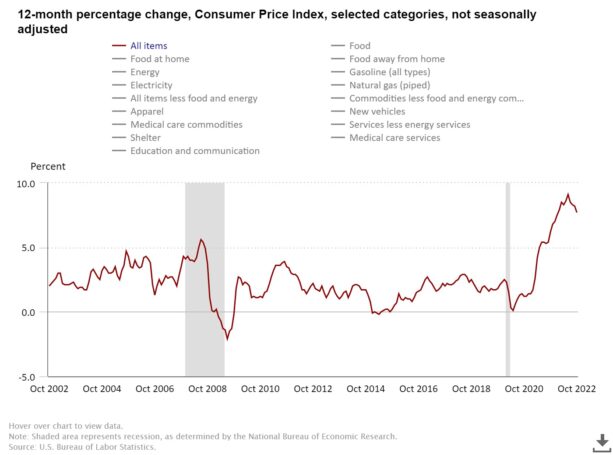

The data for this discussion is summarized in a few graphs, and their associated charts of data.

The first is the Bureau of Labor Statistics’ (BLS) 12-month percent change in the Consumer Price Index, covering selected categories of goods and services over the past 20 years. The image below shows the cumulative inflation and deflation patterns.

It is worth keeping in mind that “correlation does not prove causation.” However, carefully designed statistical experiments can demonstrate causation.

Several correlations are sharp and clear.

First: the pandemic

COVID-19 is the shock, the “externality,” that brought the economy toward collapse. It severely crippled the global supply chains upon which nearly every industry depends. Massive federal monetary and unemployment relief, and large public health interventions, stopped the plunge in economic demand.

Unlike the 2008 financial crisis and Great Recession, the financial system was not as overleveraged with fake securities, so banks and other financial institutions could be kept alive by zero interest cash. They were not forced to go bankrupt and be reorganized. 2008 was a credit crisis—bad debts were recycled as class A, until the “reckoning.” Prices fell. 2020 was a supply crisis, and, due to government intervention to sustain incomes and demand, remains a supply crisis. Prices rise.

The pandemic restructured the workforce. This is part of the “labor supply” shock, added to other shocks from the pandemic. Millions of frontline service workers’ jobs were destroyed. Most service jobs lost were lower wage, resulting in the brief rising median wage data anomaly in the first quarter of the pandemic. More of the higher wage jobs were buoyed by remote work.

Remote work and livable UI benefits kept demand for goods up. But supply did not recover quickly, including the supply of labor to meet demand. Many workers left the workforce altogether. Even now, labor supply is down. The pandemic was world wide and its impact had contradictory consequences in different parts of the world.

Remote work and livable UI benefits kept demand for goods up. But supply did not recover quickly, including the supply of labor to meet demand. Many workers left the workforce altogether. Even now, labor supply is down. The pandemic was world wide and its impact had contradictory consequences in different parts of the world.

Many contradictions flow from the private monopoly ownership of the most advanced vaccines and therapies, thus making WHO-supported demands to lift patent protections on vaccines not only a humane policy, but an economically sensible one. Parts of the pandemic’s depth and breadth globally are not entirely “external.”

Second: interest rates

The Fed began acting aggressively in June of 2021, raising interest rates and the cost of borrowing across the board.

If you follow the link to the BLS live graphic, and select the Energy graph, alone, the chart shows this began to have some effect by October 2021. However it did not, and has not yet, moved inflation anywhere near the target of 2% per year.

Russia crossed the Ukraine border in February 2022. Effectively this doubled down on the pandemic supply shock for energy while still in recovery. The removal of the world’s second largest producer from the oil and gas market put an end to the pause in inflation. This was devastating for Europe, but less so for the U.S., so far, due to the release of reserves to the market, and increased incentives (or opportunities) for shale oil production—i.e. fracked gas—to counter the fall in Russian supplies (or perhaps, to replace them). The falling rate of inflation reflects the ramped up U.S. production and reserve. The European Union Core Inflation Rate better illustrates the underlying persistent global high energy prices.

In a globalized world, sanctions generate as much or more blowback than blow. Oil stocks surged. Clean energy investments reversed, as big capital abandoned them for booming carbon profits.

The Fed then doubled down on rising interest rates—basically planning a recession aimed at triggering mass layoffs in order to discipline labor in a “too tight” labor market, with “too many strikes.” The objective was to “slow demand”—i.e. stop rising wages.

It is not slowing inflation. In fact, these anti-labor instincts are aggravating the problem. Mike Roberts has an excellent explanation for why:

Ignoring the fact that it was weak supply (blockages in transport, insufficient skilled staff and low productivity) that has been the main cause of the spike in post-pandemic inflation, Powell continued to argue that hiking interest rates would slow aggregate demand and that would bring inflation down as households and businesses reduced spending growth in the face of rising interest costs on borrowing. But this approach could only mean intensifying the hit to the supply side too—in other words, driving the U.S. economy into a slump. As Powell admitted in his speech, “Slowing demand growth should allow supply to catch up with demand and restore the balance that will yield stable prices over time. Restoring that balance is likely to require a sustained period of below-trend growth.” The words “below trend” mean recession and rising unemployment.

Third: Energy looks like the culprit. Is it?

When demand exceeds supply, prices rise. The BLS chart referenced above (when “All items” and “Energy” is selected) shows a very strong correlation to energy—which had slumped during the pandemic depression, driving the dramatic rise in prices which shortly permeated most economic sectors and industries. Energy prices rose from around 2% to 25% in less than 3 months. The release of gas reserves softened the rate rise until the Ukraine war onset, where it jumped to 40%. Of the big spike in inflation, roughly two thirds was the pandemic, and another third the Ukraine War and the associated sanctions.

However, capital investments in developing future fossil fuel resources were stagnant for most of the previous decade. Some of this reflects an investment shift toward cleaner energy. But it meant less development of new oil and gas fields. Such investments, even if successful, can take decades to return a profit. When the shock hit, oil reserves and refining capacity was not sufficient to meet demand.

The International Energy Agency reports energy investment in raw costs and power to run their own refining and production are still big factors in the overall rise in prices, which monopolies and oligopolies can pass on to consumers with impunity longer than smaller, more competitive firms. Cold War 2.0, at least with Russia, was not on the design board of Big Energy, judging by their investment patterns. But they are reaping the whirlwind now.

With the sanctions, boycotts and the shutdown of Russian gas and oil, oil corporation profits are now skyrocketing. But the recent profit history of the energy corps is not actually great compared to the overall S&P stock index. Both prices and returns on investment are historically low, according to Reuters.

Prices in the economic sectors heavily dependent on fossil fuels—especially agriculture, food, and transport—followed suit almost immediately. The removal of Russian oil and gas still makes the inflation mostly a supply shock generated by geopolitical conflict on top of the pandemic. Like the anti-labor instinct, monopoly capital’s imperialist response to the crisis only aggravates the problem. The Fed regime, slanting toward mass layoffs, will indeed bring a recession. Whether it will achieve the goal of reducing inflation is in serious doubt.

Prices in the economic sectors heavily dependent on fossil fuels—especially agriculture, food, and transport—followed suit almost immediately. The removal of Russian oil and gas still makes the inflation mostly a supply shock generated by geopolitical conflict on top of the pandemic. Like the anti-labor instinct, monopoly capital’s imperialist response to the crisis only aggravates the problem. The Fed regime, slanting toward mass layoffs, will indeed bring a recession. Whether it will achieve the goal of reducing inflation is in serious doubt.

The answer is: energy, and energy policy, is the major culprit behind inflation. A supply shock in energy leads to a supply shock in nearly everything.The challenge is, it does not appear possible to reconcile a scientific, balanced energy policy for the 21st century with the profit maximization demands of energy corporations.

Fourth: monopoly

Any market dominated by a large monopoly or oligopoly of giant firms can risk bigger inflation spikes and persistence than more competitive markets. The above graph of the inflation trend does not show that.

However, in a new report, the Federal Reserve of Boston finds that when production costs get more expensive, dominant companies pass those costs onto consumers in the form of higher prices. When industries are more concentrated and there’s less competition, that price hike becomes about 25 percentage points greater.

So, for example, if one calculates the underlying inflation components as chiefly the pandemic and Ukraine-related energy shocks, amounting to a 40% increase in prices of gas, natural gas and oil, monopoly accounts for at least 10 percentage points of the rises.

In other words, monopolies tend to overcompensate for rising production costs by jacking up their prices, exacerbating the problem. Oil and meatpacking industries are often cited as examples.

There have been numerous reforms to curb monopoly power and prerogatives for over 100 years. They include, in the first place, antitrust laws, designed to break up large firms whose pricing power and market dominance discourage competition and innovation. A classic example is the break up of AT&T, and the subsequent explosion of cellular and Internet communication technologies. Prior to break up, AT&T was a heavily regulated monopoly in most of the U.S., with guarantees by the company to provide universal service regardless of ability to pay in exchange for guaranteed rates of profit.

The breakup of Esso, the standard oil monopolies of the Rockefellers, is another historic example of anti-trust action. But, as we can see more than half a century later, the concentration of capital in fewer and fewer hands, and the gaping inequality in U.S. society was not ended by the occasional breakups of a giant firm.

There have been other efforts, besides antitrust law, to reign in monopoly and oligopoly power. Windfall profits taxes were passed in both World Wars to prevent calls for patriotic service and sacrifice from being stained by blatant corruption from military contractors.

Labor and employment laws, rent and price controls, the establishment of numerous regulatory agencies on collective bargaining, health, education, safety and environmental responsibility, were in large part all responses to the abuses of dominant corporate power. Efforts to control monopoly power also include more transparency in political contributions.

In most cases, such measures have proved temporary solutions, as big Capital continually seeks to reassert its control by evading, corrupting or re-capturing state institutions and officials. We now have the greatest concentrations of wealth and the largest inequities of our entire history.

Due to the laws of competition and maximization of profit that rule capitalist society, Capital must seek to concentrate as the scale of technologies and associated investments advance.

However, there is another material foundation to the concentration of resources. Mountain-sized obstacles need to be moved. Massive projects require big organizations and tools in order to mobilize the resources, materials, and human beings necessary to assemble them. Antitrust measures cannot finally resolve this challenge of the too-big-to-fail corporation.

Taxation could be included as an alternative reform tactic, but to achieve it, corporate and billionaire influence in elections and lobbying must be overcome. Some of the most profitable and wealthiest companies pay no taxes at all through numerous dodges, and an underfunded IRS cannot afford to investigate them all.

The contradictions and conflicts between the increasingly social nature of all production and the private accumulation of immense wealth keeps intensifying. Breaking up giant firms is at the heart of most past reforms. In many cases, this no longer makes sense. Permitting financial markets to move their investments toward fossil fuels and away from a more scientific and longer-seeing industrial policy will bring global existential damage. We need to move mountains. That means big organizations, with mountain-moving technology and a skilled workforce.

The long term solution to monopoly power in the 21st century is socialism—total or partial nationalization of firms and projects that “cannot fail” without serious public harm, or whose investment decisions cannot rest on the most and quickest profits, like Exxon and other energy giants.

Such actions are unthinkable with unfettered billionaire power and prerogatives. The ending of the monopoly component in inflation depends on the partial or complete political overthrow of monopoly power.

The overthrow of monopoly power is a central strategic concept of the Communist Party. And little does more to confirm its accuracy than the catastrophes of Trump, the pandemic, and a return to Cold War policies. But this is not a reform that billionaire-led parties can or will get done. Note the trillion-dollar Biden defense budget.

Fifth: China and Cold War 2.0

Compared with the oil and Ukraine shocks, the economic war Trump started with China—and that Biden is now escalating—are small potatoes. Bloomberg reports a likely 2-3 percentage point inflation cost embedded in U.S. tariffs and “onshoring.” The long list of “onshoring,” or “Buy America” campaigns of the past century sound good, but have never ended up in “hire Americans” (meaning, those residing in the U.S.), as far as this writer can find.

The impact of Cold War 2.0 on inflation, however, is probably a secondary consideration to the slowdown in overall growth that will result from bifurcating the economic world into U.S.-dominated zones versus anyone else that does not want to be dominated.

Far more serious even then the threat of economic slowdown and wage-hitting inflation is the threat to peace. In a bifurcated world, the supply chain problems will only be resolved through war. Given our nuclear situation, the potential implications, should we continue in the current direction, would be catastrophic.

Inflation: What it feels like to workers

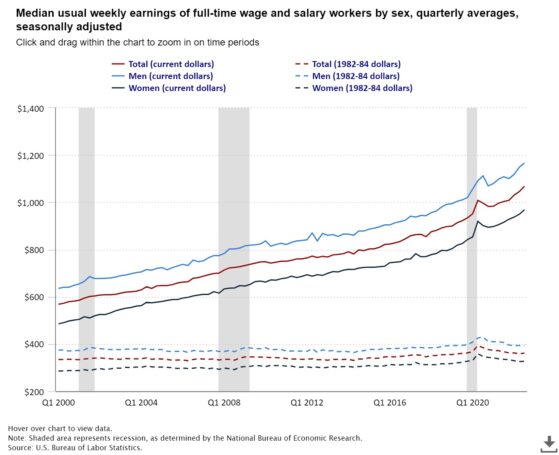

The below graph is from the BLS, and shows the median weekly earnings of men and women hourly workers since 2000. The graph strikingly shows those earnings in today’s dollars, versus the value (what it could buy) in 1982–1984 dollars.

The dotted lines are the “real” wage experiences of the median worker: flat for 20 years, and headed downward since the pandemic. The below chart gives a comparable but more detailed view of the past 5 years.

One side effect of Trump and Biden Cold War policies against China is a rise in racist attacks on Asian Americans, as well as Chinese or other Asian citizens attending U.S. universities, or performing work on H1-B visas. This is reducing the number of highly skilled graduates choosing to stay in the U.S. That impact on the “labor supply shortage” is not included in the Cold War 2.0 inflation factors. Similarly, efforts to close the border to immigrants limit the options to increase the labor supply.

The quit rate spiked as demand for workers rose, and nominal wages began to rise, especially in frontline occupations, but not real wages—not enough for most to keep up with inflation.

Wage increases are not causing inflation

Former Treasury Secretary Lawrence Summers and others have blamed rising inflation, in part, on rising worker wages. Frankly, this is a contemptible position, given the past 40 years of rising inequality. But Wharton professor Jeremy Siegel has the best response I have seen, from Business Insider:

“We had 5% year-over-year wage growth. We have 8% inflation. Workers are trying to catch up and they’re not. They’re still falling well behind. It just disturbs me to think that the Fed policy is to crush wages so they go back down to 2%, basically saying to the worker, ‘You’re not going to catch up to inflation, and we’re going to prevent you from catching up to inflation.’ That’s an insane policy.”

Inflation hurts workers when wages don’t keep up. It hurts lower and median wage workers perhaps worse, and those—including millions of women—left at home when the pandemic crashed child care services, and death struck the home. Many have not been able to return to the workforce, now changed by a pandemic of increased racism, misogyny, immigrant bashing, mass murders, intolerable pandemic working conditions in health care, manufacturing, emergency services, infrastructure, transport, and more. Inflation made net incomes fall 3% in value this year alone.

The inflation topic is a complex one with many impacts. As it persists, so do people’s expectations that it will continue to rise, which will result in another collapse of demand. There are many systemic features of modern U.S. capitalism that bear on it: monopoly-driven, imperialist foreign policies, the gaping inequalities permeating U.S. society, the spreading political dysfunction of the two-party system, the dangers of over-financialization, and more. In such circumstances, triaging and prioritizing the possible from the impossible is the best one can do to find the path forward.

One choice is to “let the market decide.” That would be the billionaires’ position (who, in reality, are currently setting the rules of the market). Right now, “the market’s” advice is to have a recession and double down on investments in fossil fuels.

Then there is the “socialism” solution, which would mean radical reform of the political system to prevent continued domination by billionaires. That would deal with the monopoly problem, in theory, but does not look like an immediately available solution, to this writer.

That leaves us with the takeaways from the opening of this piece. Bring the Ukraine war to a halt—which means, stop the flow of weapons to Eastern Europe, and negotiate. Abandon the Cold Wars for cooperation and collaboration to repair the damage from the pandemic.

Develop a serious campaign to nationalize the commanding heights of energy infrastructure. Push forward on industrial policies that a) raise real wages in proportion to value creation; b) find something for everyone to do; c) leave no one behind.

The problem of monopoly must be addressed for a sustainable solution and a positive economic outlook. No billionaire-led party has any incentive to make such changes. It is hard to avoid the conclusion that an independent political formation must emerge. Such a formation can only emerge out of the mass working class and people’s movement.

The opinions of the author do not necessarily reflect the positions of the CPUSA.

Images: United States one-hundred-dollar bill by Farsnews.ir / Mohammad Mahdi Durrani (Creative Commons Attribution 4.0 International License); Life in the Time of Covid by Billie Grace Ward (CC BY 2.0); Plastic bottles and garbage on the bank of a river by Horia Varlan (CC BY 2.0); 12-month percentage change, Consumer Price Index, selected categories by Bureau of Labor Statistics (Screenshot); People’s Unemployment Line by Joe Piette (CC BY-NC-SA 2.0); Protest against COVID vaccine patents by AIDS Healthcare Foundation (Facebook); Baristas on strike (Twin Cities CPUSA on Twitter); Claas Lexion 750 Combine Harvester by Martin Pettitt (CC BY 2.0); Tax the Rich (for once) by Chuck Olsen / Chuckumentary (CC BY-NC-SA 2.0); Median usual weekly earnings of full-time wage and salary workers by sex by Bureau of Labor Statistics (Screenshot); Real average hourly earnings decreased 2.8 percent from October 2021 to October 2022 by Bureau of Labor Statistics (Screenshot);

Join Now

Join Now{kind=link}